# United States Deep Ultraviolet (DUV) Lithography for Superconducting Qubit Patterning Market Insights

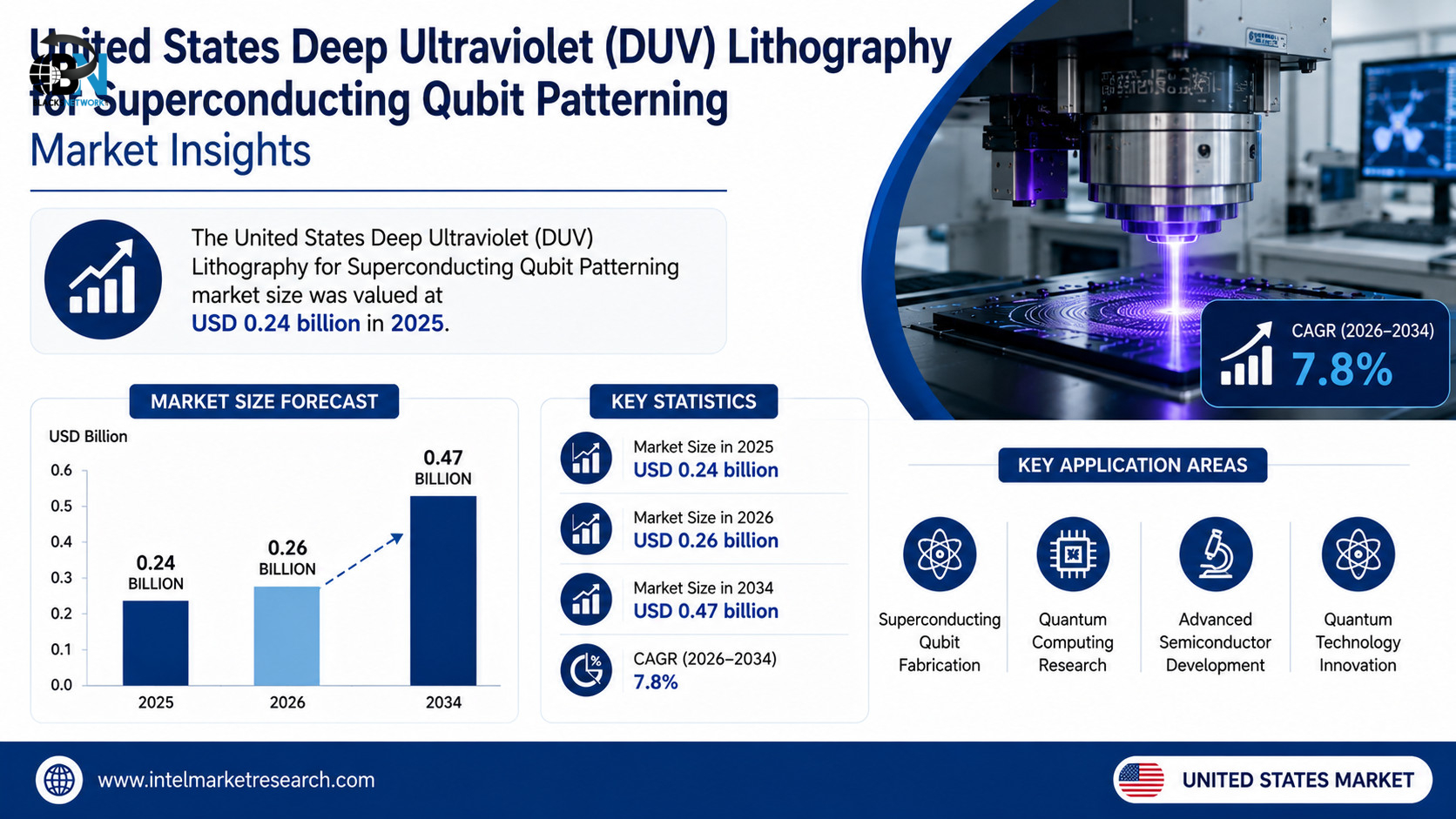

The **United States Deep Ultraviolet (DUV) Lithography for Superconducting Qubit Patterning Market** was valued at **USD 0.24 billion in 2025** and is projected to grow to **USD 0.47 billion by 2034**, registering a **CAGR of 7.8%** during the forecast period. The market is expanding rapidly due to increasing investments in quantum computing, government funding initiatives, and advancements in semiconductor manufacturing technologies.

Deep Ultraviolet (DUV) lithography uses wavelengths between **193 nm and 248 nm** to create highly precise semiconductor patterns. In superconducting qubit fabrication, the technology is essential for manufacturing **Josephson junctions, resonators, and interconnects** with extremely low defect rates. Its ability to produce sub-100 nm features makes DUV lithography a critical technology for building scalable and high-performance quantum processors.

The market is primarily driven by strong federal support through initiatives such as the **National Quantum Initiative**, along with growing investments from both public and private sectors. Collaborations between leading research institutions, semiconductor manufacturers, and quantum computing companies are accelerating the commercialization of quantum hardware and expanding demand for advanced lithography solutions.

Technological innovation continues to strengthen market growth. Advances in **193 nm DUV systems, high-NA optics, advanced photoresists, and precision mask technologies** have significantly improved pattern accuracy, throughput, and manufacturing efficiency. These developments are enabling manufacturers to produce increasingly complex superconducting qubit architectures while maintaining high quantum coherence.

Despite strong growth prospects, the market faces challenges including the **high capital cost of DUV lithography systems**, limited availability of specialized materials such as ultra-pure photoresists and quartz optics, and strict regulatory and safety requirements. However, government incentives aimed at strengthening domestic semiconductor manufacturing and localized supply chains are expected to reduce these barriers over time.

Emerging opportunities include the integration of DUV lithography with **cryogenic packaging technologies**, expansion of domestic photoresist manufacturing, and strategic partnerships between equipment manufacturers and quantum hardware developers. These developments are expected to improve production efficiency, reduce manufacturing costs, and accelerate commercialization of next-generation quantum computing systems.

Major companies operating in the market include **ASML Holding, Applied Materials, Lam Research, JSR Corporation, Tokyo Ohka Kogyo (TOK), IBM Quantum, Google Quantum AI, Rigetti Computing, Quantinuum, Microsoft Quantum, Intel, Canon, SCREEN Semiconductor Solutions, and MIT Lincoln Laboratory**. These organizations continue to invest heavily in research, product innovation, and strategic collaborations to strengthen their leadership in the rapidly evolving quantum computing ecosystem.

**Get Full Report Here*

https://www.intelmarketresearc....h.com/semiconductor-

1 (877) 773-1002

1 (877) 773-1002